)

July monthly letter | “Going for gold”

Elements is AuAg's monthly letter highlighting macroeconomic observations from the previous month. Our focus is on events that impact the investment environment for gold, silver and other essential metals. These observations are presented with images and charts laid out efficiently and concisely.

Au and Ag in the past month

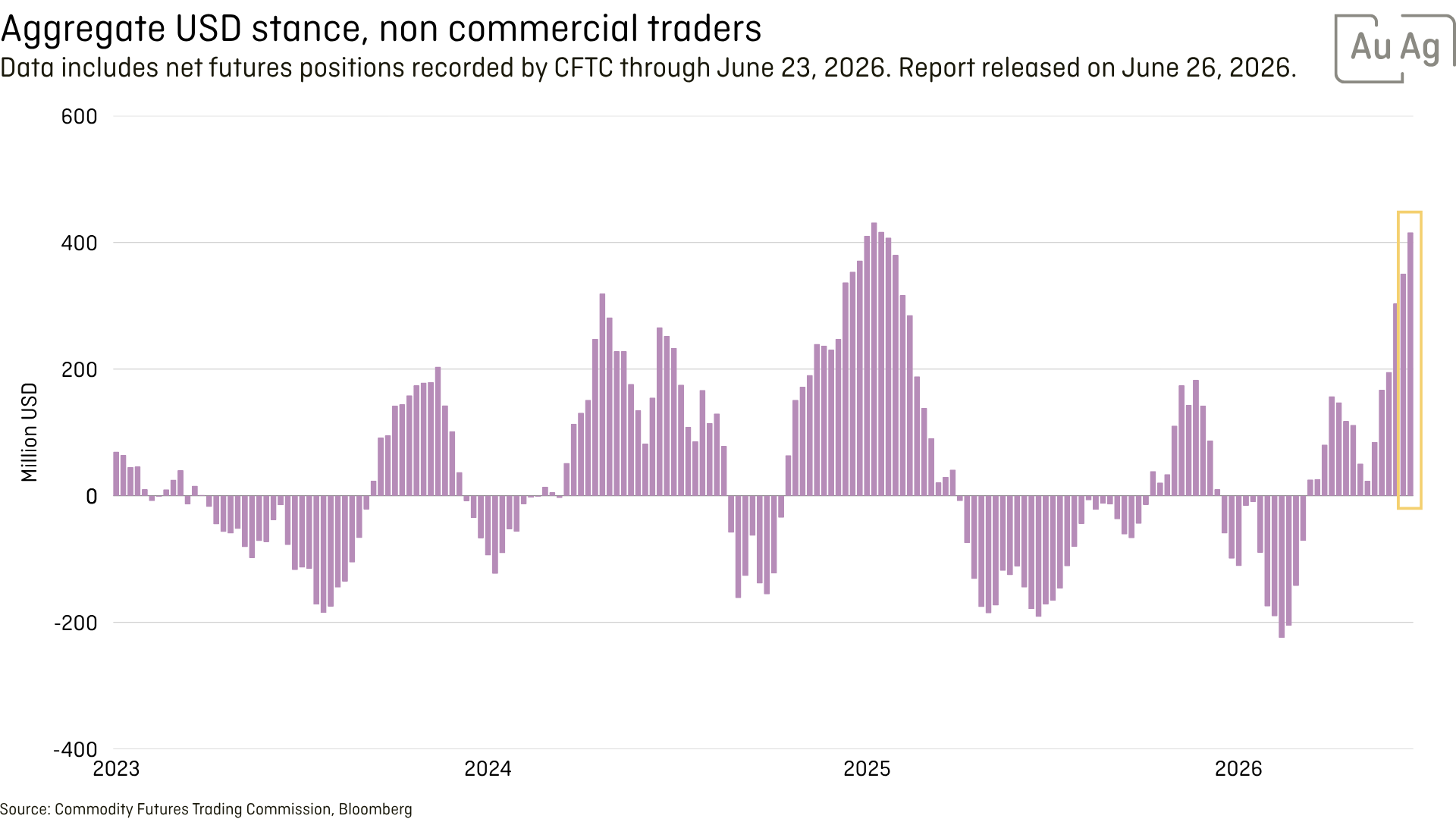

Market expectations of Fed rate hikes have, over the past few months, pushed many toward the dollar, creating a clear headwind for gold. Gold ended the month at USD 4,007 per troy ounce, down −11.7% from USD 4,540. At the same time, the dollar index has risen sharply and the dollar is now extremely overbought — a setup that likely will lead to a reversal going forward.

Underlying factors (debt reaching new record highs and enormous budget deficits with more and more unfunded projects) continue to be strong fundamental drivers for materially higher gold prices.

Underlying factors (debt reaching new record highs and enormous budget deficits with more and more unfunded projects) continue to be strong fundamental drivers for materially higher gold prices.

As soon as the market also recognizes the difficulty of raising rates into a “cost-push inflation,” and that the U.S. simultaneously has to bring long-term rates down, a new trend for the gold price will take off again. It is precisely the level of long-term rates that makes the cost of America’s enormous debt such a heavy burden.

At the same time, following confiscations and trade wars, many countries are now showing less interest in buying U.S. Treasuries. The Iran war has also hurt several Arab countries, countries that had expected more of the promised protection under the Petrodollar arrangement. Combined with reduced oil production and lower trade surpluses, further purchasing power is disappearing. That makes it harder for the U.S. to keep financing its ongoing budget deficits.

To press long-term rates lower, an excess of bond buyers is needed. If that demand isn’t there in the market, the Fed will have to step in as “the buyer of last resort.” Once we see some form of quantitative easing again, gold prices will rise to new all-time highs (above USD 5,594 per troy ounce). With the mid-year mark behind us, we may be at the start of that move. Once it takes off, many will be surprised how quickly it can travel.

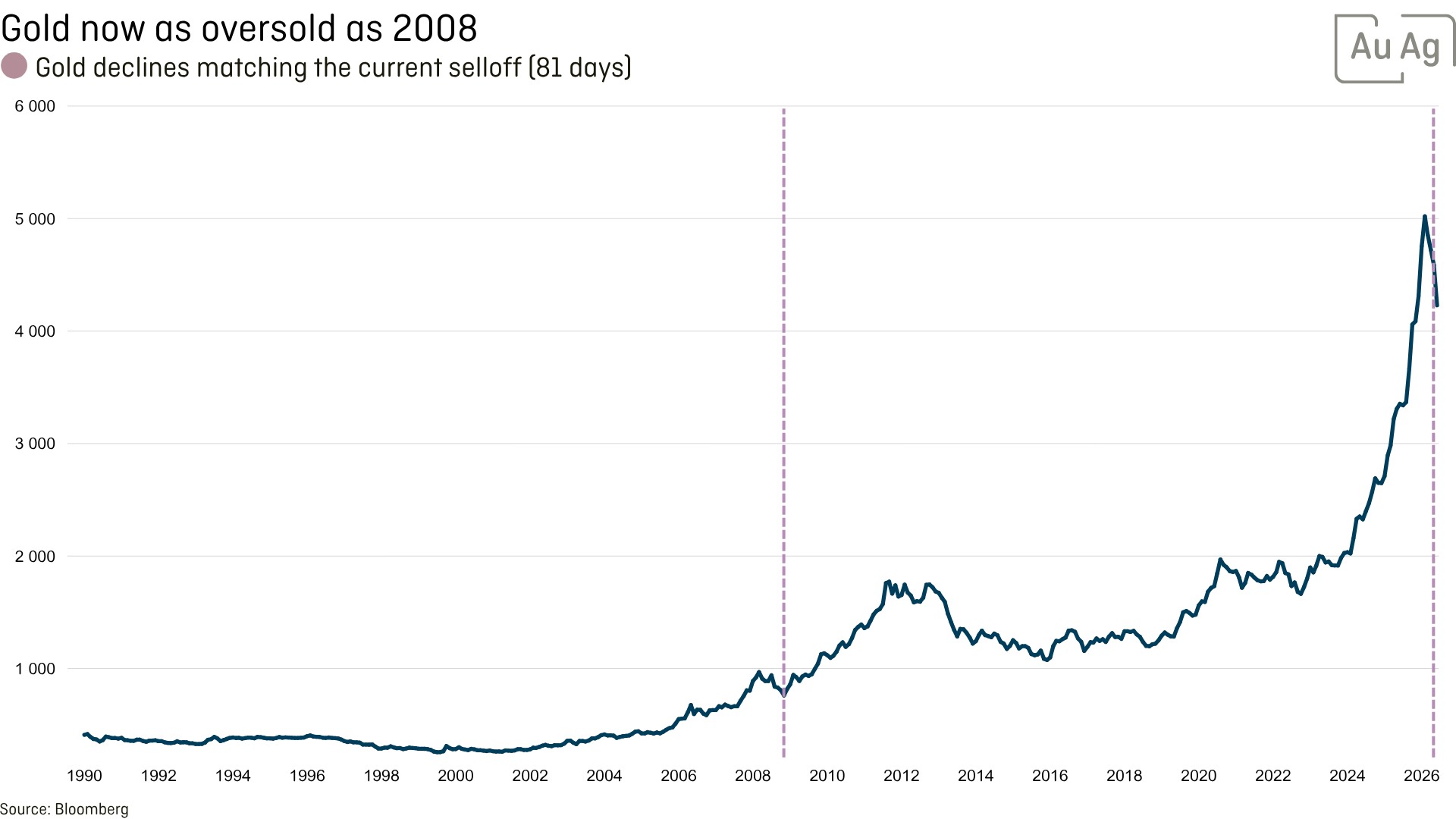

Gold is now also as oversold as it was during the financial and debt crisis of 2008. As always, after long periods of rising prices, sharp corrections of 20–30% are normal before the next upswing takes hold.

Gold is now also as oversold as it was during the financial and debt crisis of 2008. As always, after long periods of rising prices, sharp corrections of 20–30% are normal before the next upswing takes hold.

Gold Price per Troy-Ounce (oz) in USD

The silver price closed at USD 58.61 (USD 75.40), a sharp −22.2% decline and levels we haven’t seen since December 2025. Silver, like gold, has been affected by the algorithmic trading that has dominated the market since the war against Iran began. For silver, the setup going into the autumn is at least as strong — perhaps even stronger. The correction has been larger, which is also natural for a more volatile commodity.

Silver Price per Troy-Ounce (oz) in USD

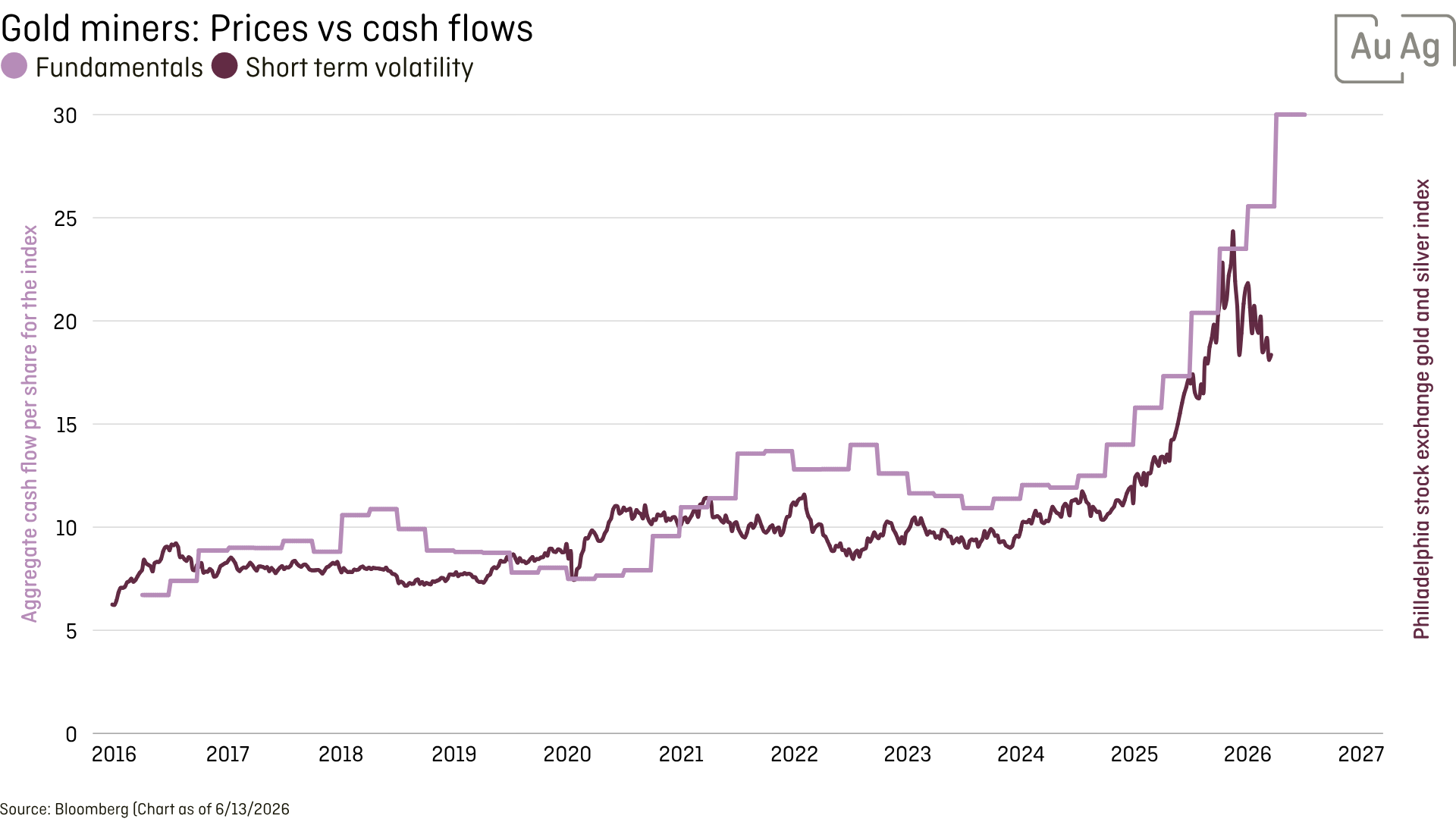

The mining companies (as viewed through the funds) outperformed the metals themselves in June — a sign of strength, and an indication that the correction moves in gold and silver are expected to be temporary in nature. We’ve already seen the first signs that the Fed is starting to strike a softer tone. When the market catches on, both the commodities and the companies will start moving strongly again. It is also clear that it isn’t the companies’ fundamentals (such as cash-flow trends) that have driven recent price action.

The AuAg funds - Highlights

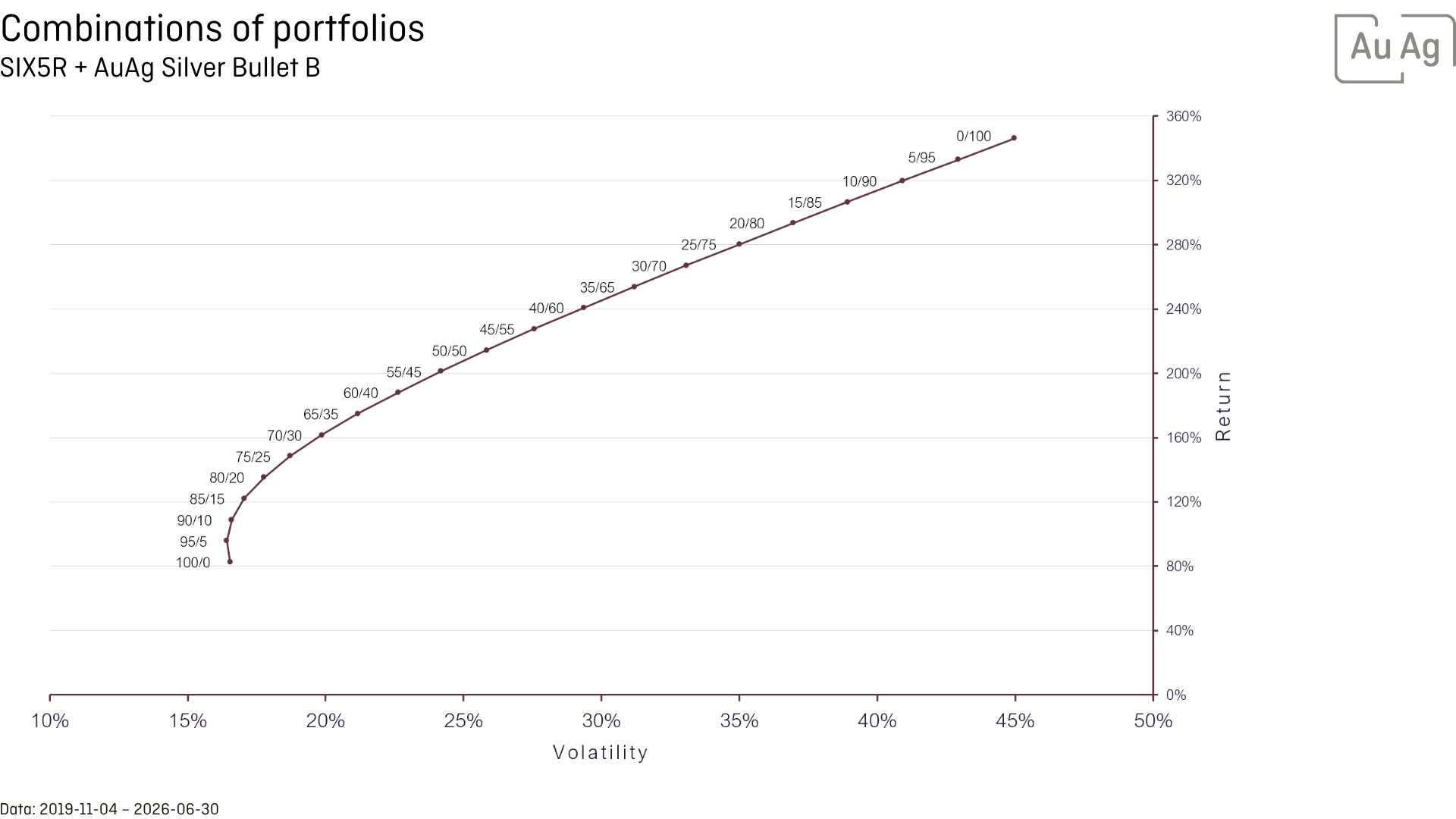

AuAg Silver Bullet is the market’s most volatile precious metals fund and, as such, is expected to move the most on the upside and the downside among all the funds in the sector. That AuAg Silver Bullet was the best-performing fund across all categories in 2025 was perhaps not so surprising, but it is all the more remarkable that the fund is also the best of all precious metals funds so far this year. That is genuinely strong and bodes well going into the second half of 2026. We would not be surprised to see the fund — top-ranked on 3-year returns across all funds (+239.06%) — continue to demonstrate its character when the gold and silver market turns back up.

Our first fund, which has weathered the Covid crash, the fastest rate-hiking cycle in modern history, the Ukraine war, and now the Iran war too, has an impressive CAGR (Compound Annual Growth Rate) of 22.61%. Combined with a low correlation (0.23) to the “regular” equity market, the fund is also an optimal tool in any fund portfolio.

Keep in mind that all our funds carry high volatility, and AuAg Silver Bullet is also known as “Europe’s riskiest fund.” Volatility can feel uncomfortable, but at the same time it’s what makes fund investing exciting. It is of course an advantage to have steady nerves and not sell at the wrong times. As we’ve said before, if you can’t hold the position all the way through, you can always trim a little (say 5–10% at each upswing) and buy back the equivalent on the way down.

If you make volatility your friend, you can actually earn a higher return than if the fund simply moved up in a straight line.

Global Outlook with AuAg

In the introduction we wrote about the dollar’s temporary rally, driven by offensive USD positioning in the currency market. That move has spilled into several markets. Now that the Fed is starting to signal a softer line than the market had previously priced in, we see a sharp reversal ahead, which will give both gold and silver significant tailwinds.

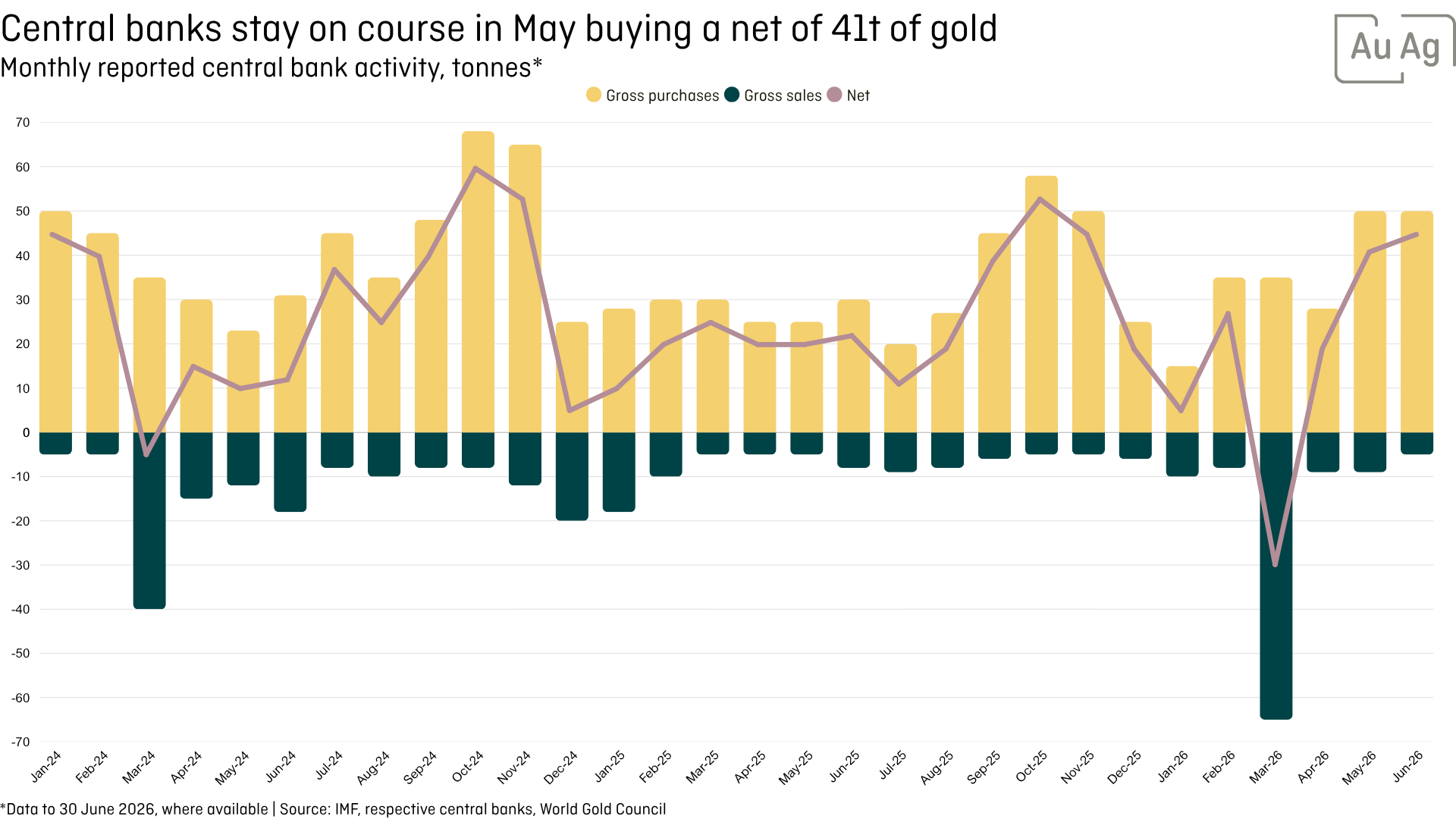

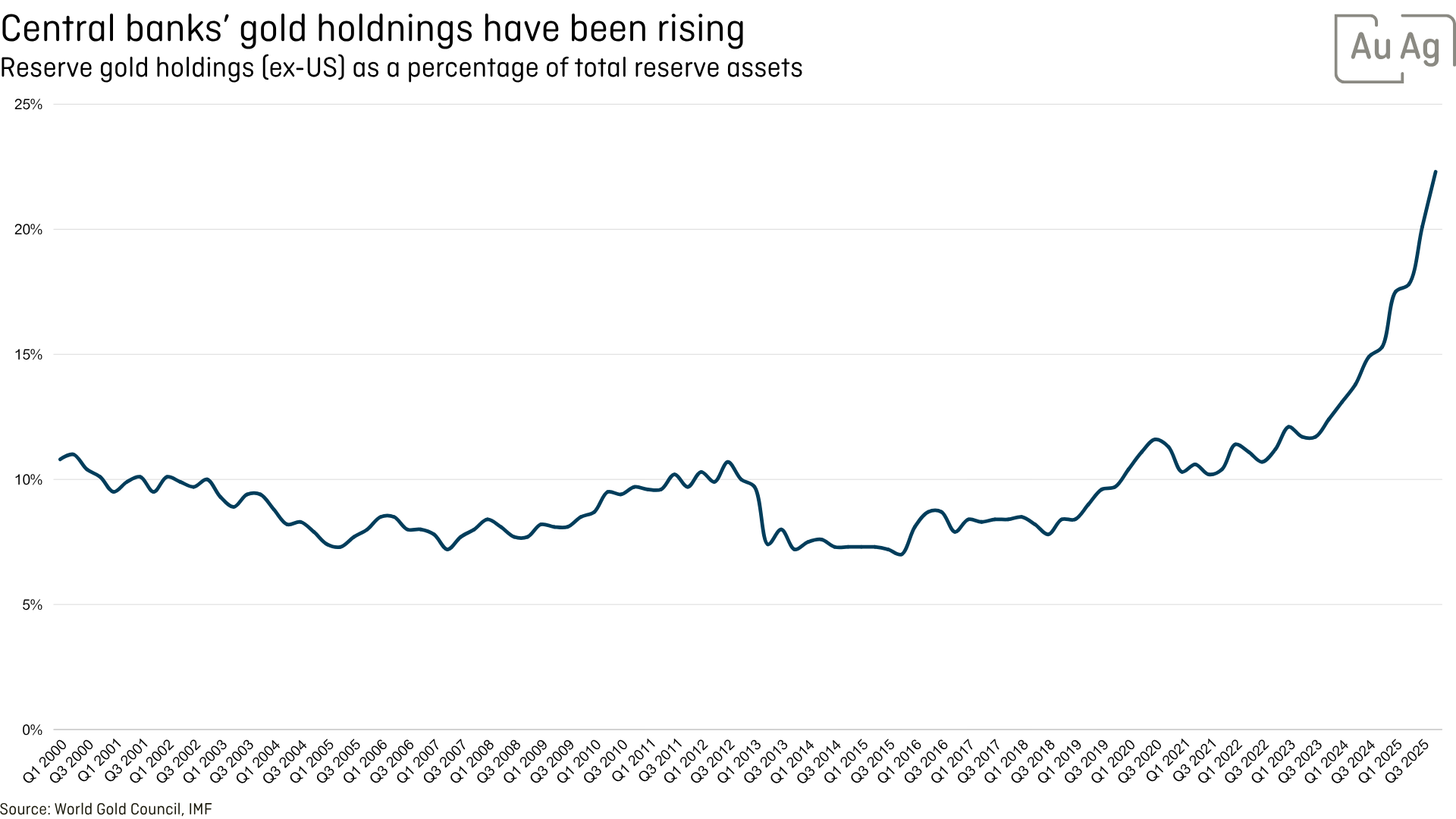

Central banks have been large net buyers of gold since 2011, and the trend has continued through the first half of 2026.

One might think that after 15 years of buying, central banks would start selling parts of their gold. But the more accurate read is that this is a trend that has begun — and that central banks see a strong need for an asset with no counterparty risk, and one that cannot, unlike U.S. Treasuries, be used as a lever of power by another party.

We take note of the large capital flows into IPOs, and above all SpaceX. It’s unique for new companies to come in already as mega-caps and become a significant part of the index, rather than, as traditionally, growing gradually into the top 100. In space there are black holes… and we’ll see how this affects all index allocations now that other tech companies will make up a smaller share of the index.

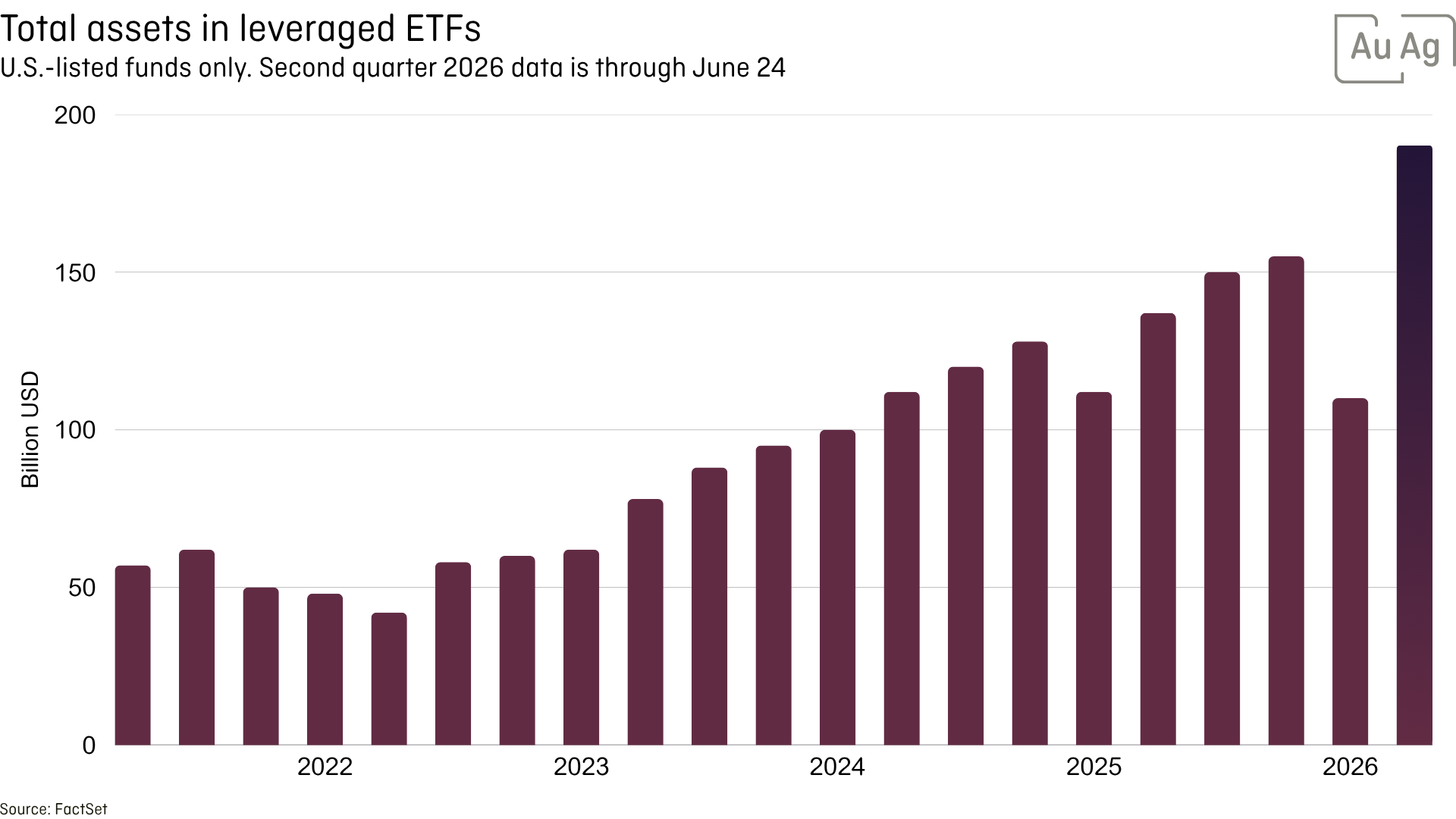

Alongside these capital flows, we also note that capital in leveraged products is growing at a worrying pace. These products risk turning the stock market into something of a casino, rather than a place where investments are made on the basis of valuations and without leverage. That could produce significant volatility down the road.

Now in the summer months, many people may have time to relax in the hammock and follow the sporting calendar. The football World Cup is heating up, and soon the winner will get to lift the trophy that everyone plays for. Going for gold, you might say, because the winner’s trophy that symbolises the best is of course made of gold. The trophy itself weighs 6.175 kg, of which 5 kg is 18-karat (75%) gold.

The designer, Gazzaniga, described his vision with the words: “The lines spring out from the base, rising in spirals, stretching out to receive the world. From the remarkable dynamic tensions of the compact body of the sculpture rise the figures of two athletes at the stirring moment of victory.” That description captures the trophy’s essence perfectly. Look at it closely and you can see exactly what he meant: two stylised human figures rise from a spiralling base, arms outstretched, holding the Earth itself at the peak. The figures are deliberately abstract — they represent athletes universally, any nation, any player, any champion.

Disclaimer

This material is marketing communication. The information does not constitute investment advice or a personal recommendation. Investment decisions should be based on the fund’s information brochure and fact sheet, as well as your own considerations. Investments involve risk. Past performance is not a guarantee of future returns. The money invested in the fund may both increase and decrease in value, and it is not certain that you will recover the entire amount invested. Before making an investment decision, you should review the fund’s information brochure and fact sheet, available under Documents on the respective fund page.

Be part of the journey

More than 100,000 investors across Europe have invested in the AuAg funds.

)

)

)

)

Featured content this month

Explore our "Research centre" to take part in our current view of the market and the macro environment. We continuously update with new articles and publications. Here are some of the latest entries:

)

)