)

“Silver is for champions”

Elements is AuAg's monthly letter highlighting macroeconomic observations from the previous month. Our focus is on events that impact the investment environment for gold, silver and other essential metals. These observations are presented with images and charts laid out efficiently and concisely.

Intro

January began the year with historical levels for both gold and silver. In this monthly update, we review recent developments in the market for metals and mining companies, as well as outline what we can expect from the rest of this month. December closed with a show of strength in precious metals, with gold and silver reaching new all-time highs of USD 4,549 and USD 83.77 per troy ounce, respectively — levels never previously seen.

Later this month, we will also publish our updated outlooks for gold, silver, and mining companies. These will take a closer look at key drivers, risks, and our expectations for 2026.

Au and Ag during the previous month

The gold price closed the month and the year at USD 4,315 (USD 4,230), rising a further +2.0%. This resulted in a full-year increase for 2025 (in USD) of +64.4%.

Once again, we saw a new all-time high on 26 December: USD 4,549 per troy ounce. Gold at USD 5,000 doesn’t feel like it’s that far away anymore.

Silver had a very volatile, but exceptionally strong month, closing December at USD 71.31 (USD 56.44). The silver price rose +26.3%, significantly outperforming gold. The final surge in December meant that silver’s full-year return for 2025 in USD came to +146.6%.

We also saw a new all-time high during the extremely turbulent post-Christmas period: USD 83.77 per troy ounce. As we previously wrote, we should expect swings of more than 10% in both directions. The moves were perhaps unusually large this time, partly due to the many public holidays and the difference between Swedish/European holidays and US trading days. From mid-January, we expect clearer signals on price direction as markets become deeper and more liquid.

2026 may well be the year when silver reaches a triple-digit price, above USD 100 per troy ounce. This is a major milestone on the way to our longer-term target over the coming years: USD 300.

So, is silver better than gold? Well, silver not only outperformed gold, but it is also truly the metal of champions. It has been since antiquity, representing excellence and achievement. Sports trophies across the world are, in principle, made of silver. Including winners’ trophies such as the NHL Stanley Cup, NFL Super Bowl, Baseball World Series, National Basketball competitions, the America’s Cup, Wimbledon, the French Open, and the PGA US Open. Over the coming year, a new generation of athletes will compete for the very top and fulfil their dreams of lifting the champions’ trophies high, just as those before them did. The reward for being the best will be: silver.

Gold, silver, and diversified mining companies clearly outperformed the underlying commodities in 2025. The AuAg funds delivered the following returns in USD:

- AuAg Gold Rush (USD): +131.85% (+104.30% in SEK, +116.20% in EUR)

- AuAg Silver Bullet (USD): +223.95% (+163.72% in SEK, +179.97% in EUR)

- AuAg Essential Metals (USD): +80.11% (+53.43% in SEK, +63.29% in EUR)

The leverage of mining equities compared to the underlying metals has, as many have noticed, varied significantly during different periods of the year. We saw the sharp rally in the companies cool towards the end of 2025, even as silver prices surged. This brought many investors to express concern and ask why mining shares didn’t have a sharper rise, given a silver price of USD 70–80. This is quite natural, though. When the commodity prices rise so quickly, many assume that the current level isn’t sustainable, and that it may simply be a bubble. If silver were to drop rapidly back towards USD 50, the mining companies wouldn’t have had time to benefit materially from the higher price. That is the simple explanation for what we have seen recently.

For those who reflect on this, it can instead be viewed as an opportunity. The situation benefits investors who dare (as we do) to believe that this is only the beginning for silver, and that it is once again possible to buy these companies at a meaningful discount. In fact, from a valuation perspective, the companies have become cheaper despite their strong gains in 2025. It is hard to imagine better conditions going into 2026.

The AuAg Funds - Highlights

With all funds ranked among the top 15 over the year, it would be easy to highlight every single one. But first place is first place, and AuAg Silver Bullet went all the way to the top, outperforming over 15 00 funds listed on online brokerage platforms. With a return of +10.7% in December, the fund finished the year at +163.72% in Swedish kronor. This has received substantial media attention, most recently in an article on Placera.

We’ve said from the start that this fund is expected to deliver several years of triple-digit returns. This has been the first of those years, and a lot suggests that 2026 could be just as strong.

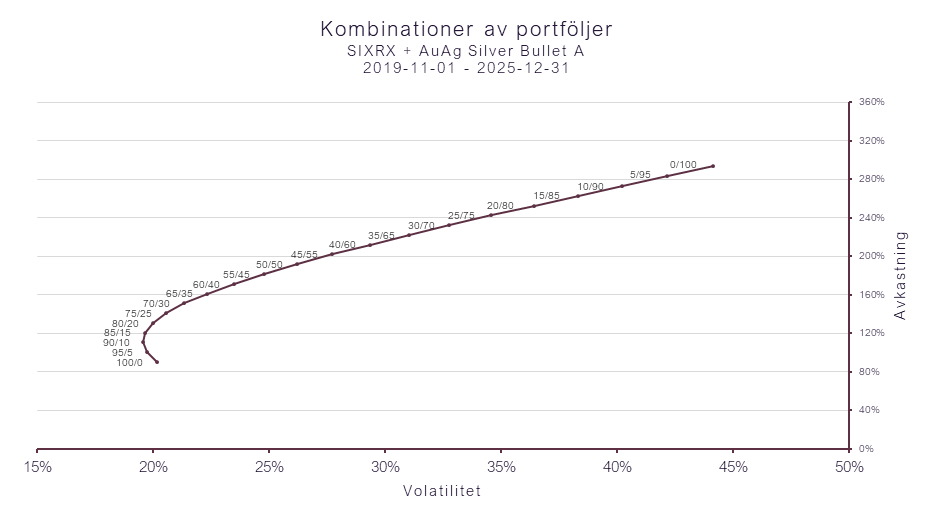

Regarding portfolio construction, we have also produced a chart that showed it has been better to hold 10% AuAg Silver Bullet and 90% Swedish equities (measured by SIXRX) — than to hold 100% Swedish equities alone. Both in terms of returns and volatility/risk.

Though it can’t be denied that going 100% in AuAg Silver Bullet has been the most profitable option… provided one was willing to accept the higher risk.

Global perspectives with AuAg

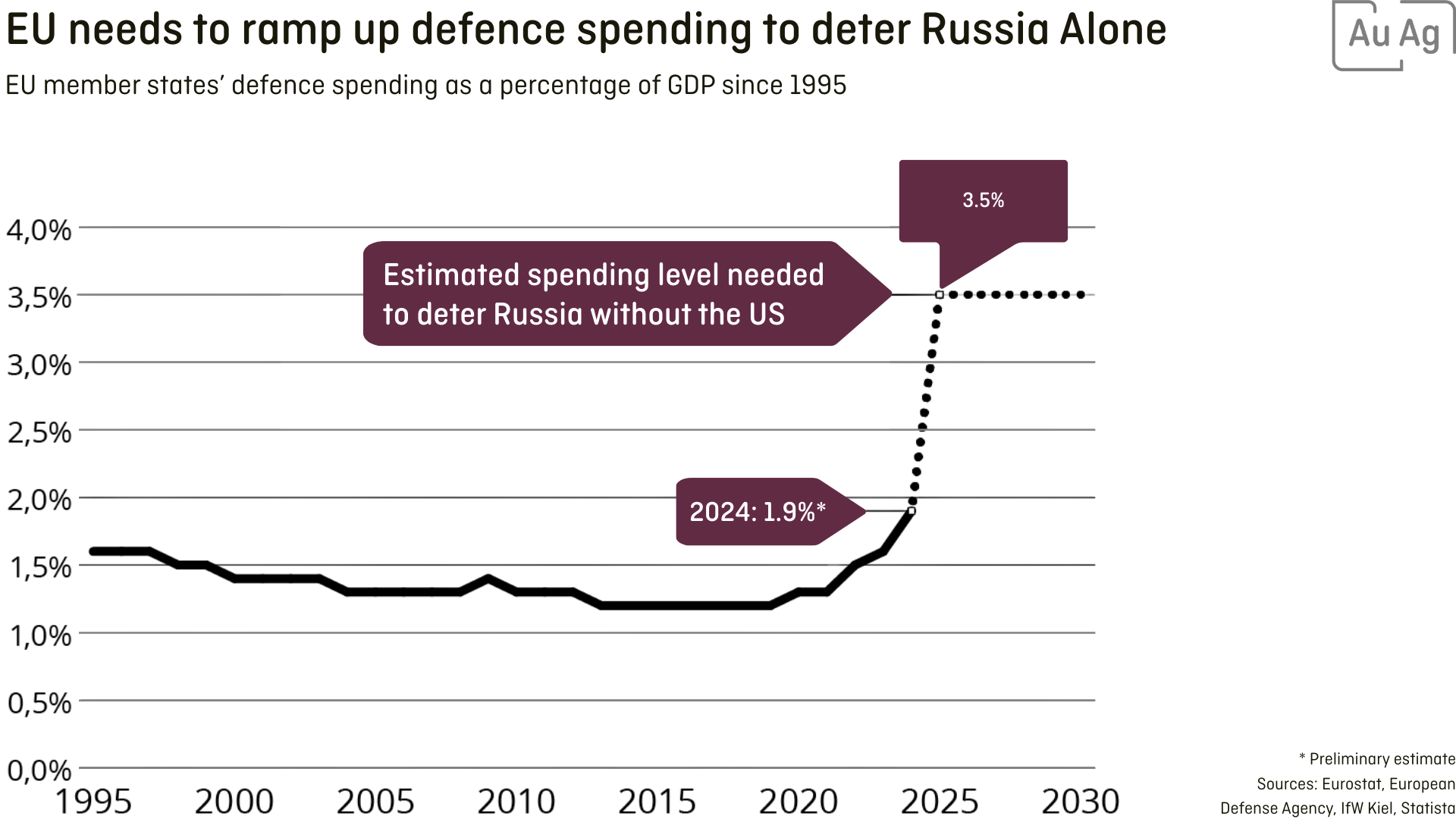

If global macro lately isn’t primarily about interest rates and central banks, then it is about how the US acts as the World Police. Europe remains on the sidelines, while Chile and Russia continue to gain increased confidence to act more assertively from a military perspective. Although the US action in Venezuela took place in January, it still warrants attention in this newsletter, which is being published slightly later than usual due to the holiday period.

The world is set to produce far more weapons going forward, in stark contrast to the disarmament we have seen for many years. Even though this (once again unfunded) expansion will technically appear as an increase in GDP, it feels like an accounting exercise: it is relatively non-productive GDP growth from a societal point of view. Moreover, it is an investment that cannot be financed through direct taxation — it must be funded through increased borrowing. That leads to more monetary units in the financial system and fuels monetary inflation. Which, in turn, provides another driver for continued increases in gold and silver prices.

The world is set to produce far more weapons going forward, in stark contrast to the disarmament we have seen for many years. Even though this (once again unfunded) expansion will technically appear as an increase in GDP, it feels like an accounting exercise: it is relatively non-productive GDP growth from a societal point of view. Moreover, it is an investment that cannot be financed through direct taxation — it must be funded through increased borrowing. That leads to more monetary units in the financial system and fuels monetary inflation. Which, in turn, provides another driver for continued increases in gold and silver prices.

Since all weapons and military systems are built from metals, rising defence spending will also lift demand — and prices — across a broad range of metals. In that sense, metals are the “picks and shovels” of the defence build-up.

As we wrap up an outstanding AuAg 2025, we look ahead with curiosity to the developments that will influence metal prices and equity markets in 2026. But more on this in our Outlook, to be released later this month.

Disclaimer:

AuAg publishes product-related information only and does not provide investment recommendations. Past performance is not a guarantee of future returns. The value of fund investments may rise or fall, and you may not get back the full amount invested.

Be part of the journey

More than 100,000 investors across Europe have invested in the AuAg funds.

)

)

)

)

Featured content this month

Use our unique "Research Centre" on an ongoing basis to take part in our current view of the market and the macro environment. We communicate all the time. Here are a few media links from the past month:

)

)

)