)

“He who has the gold makes the rules”

Elements is AuAg's monthly letter highlighting macroeconomic observations from the previous month. Our focus is on events that impact the investment environment for gold, silver and other essential metals. These observations are presented with images and charts laid out efficiently and concisely.

Intro

During the month of July, both gold and silver prices have consolidated around previous levels. The market has been focused on tariffs, Trump, and the lack of clear signals from the Fed. Many major banks have now once again begun raising their gold price forecasts, something we at AuAg already did in our outlook for 2025. More on this in this month’s letter below.

Gold and Silver during the previous month

The gold price ended the month at USD 3,290 (3,305), remaining almost exactly at the same level as one and two months ago (-0.4%). Gold did not set a new all-time high in July, but, like the previous month, it temporarily rose above USD 3,430 per troy ounce—only USD 70 shy of the record.

Gold has now been consolidating for over three long months, with weak hands selling and strong hands buying. We may approach the next upward phase, potentially targeting the USD 3,600–4,000 per troy ounce range. Perhaps the rally begins now—in the golden month of Au-gust. With the Fed’s non-decision in July (leaving interest rates unchanged) behind us, the focus now shifts to what will be “communicated” during the Jackson Hole Economic Policy Symposium, taking place August 21–23.

The silver price ended July at USD 36.72 (36.12), marking only a slight increase (+1.6%). However, the rise was much more significant earlier in the month, with the price nearing USD 40 per troy ounce on July 23. From the July peak of 39.53, the price retreated down to the 36–37 USD range.

The Gold/Silver Ratio (GSR) is now just below 90. Our forecast of gold reaching USD 3,300 has already been achieved. However, we also look forward to a GSR of 70, with gold at 3,300, implying a silver price of USD 47 per troy ounce by year-end. We’ve also been clear that gold below 4,000—and even below 4,300—is undervalued. We’ve pointed this out as early as September 2024, and it has also been highlighted in the media in March, April, and June 2025. Major players like Fidelity and JPMorgan are targeting 4,000 (+20% from today) as the next major milestone. At a GSR of 70, silver would reach USD 57 per troy ounce (+54% from today).

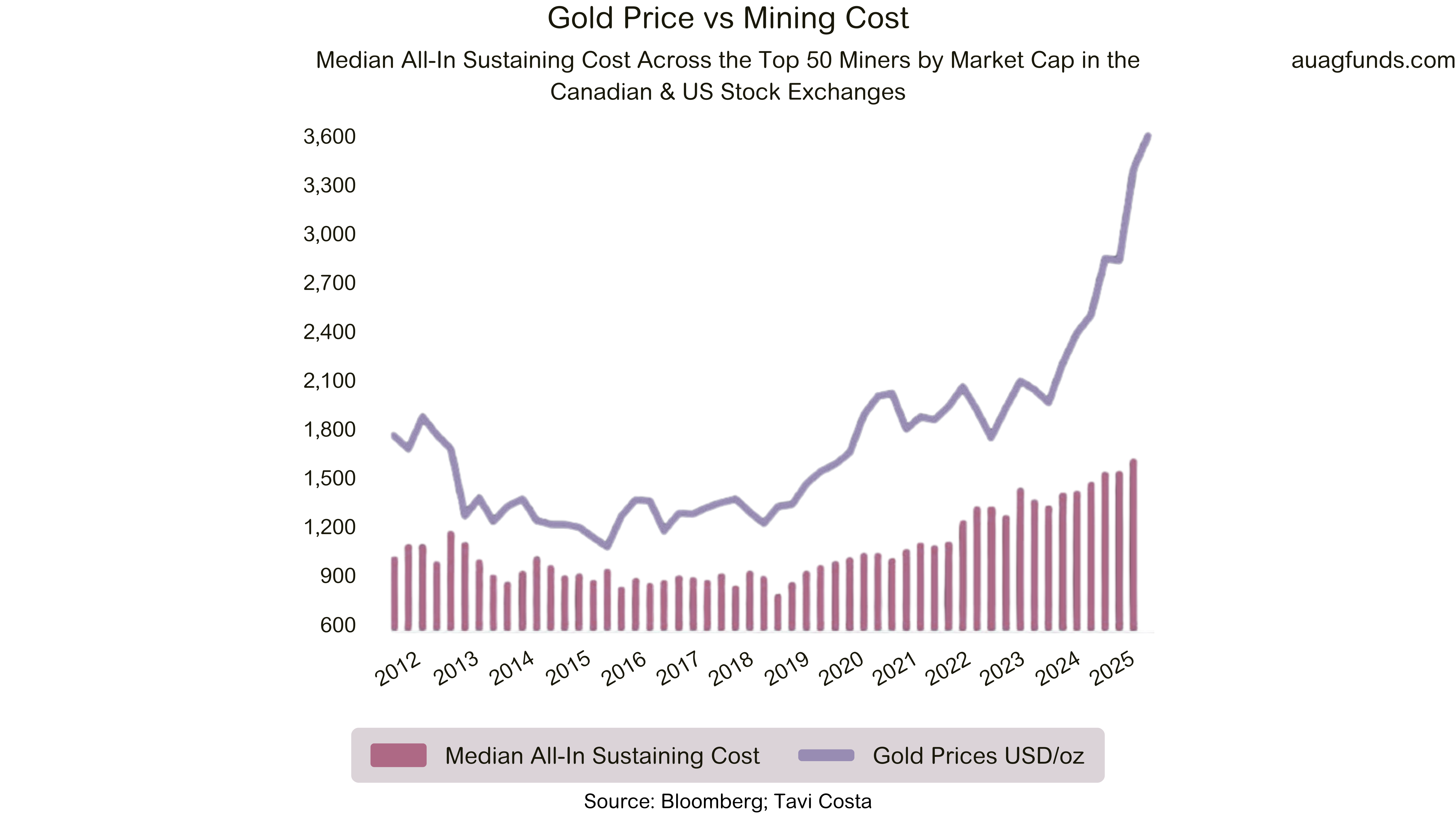

Historically, gold has shown strong seasonal performance in the fall, starting with the “gold month” of Au-gust. Let’s see if that pattern holds this year as well. Among the companies in the sector, we recently saw the giant Newmont deliver a very strong Q2 2025 earnings report, well above analyst consensus. This bodes well for continued strength across the entire sector.

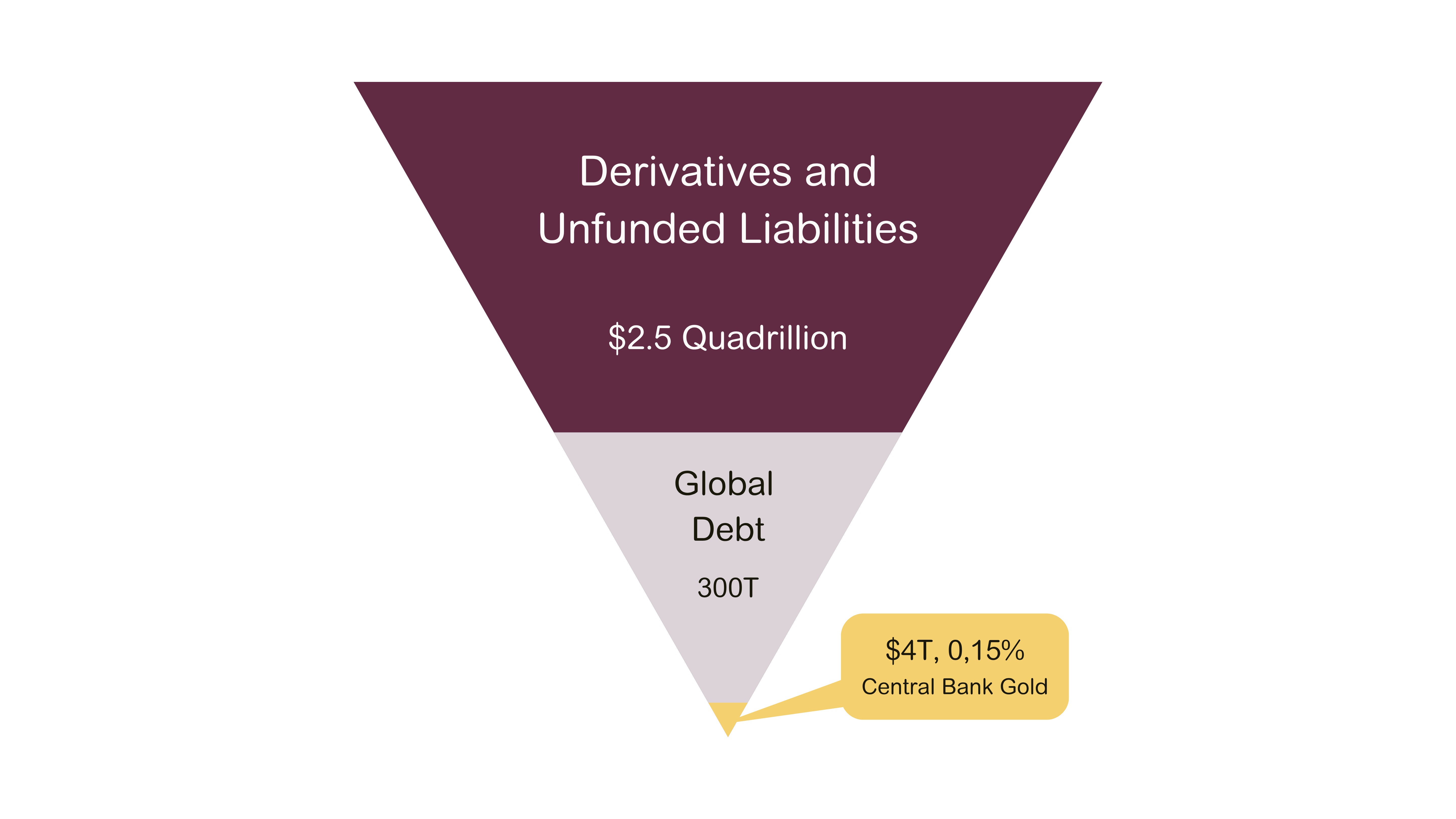

Lately, we’ve noticed that Trump frequently uses gold-toned furniture as a backdrop at his events, and more often replaces his red or blue tie with a gold one. The saying “He who has the gold makes the rules” is one that Trump would likely want to use to support his agenda. Central banks’ gold reserves continue to play a significant role in providing stability in a world burdened with enormous debt, massive derivative exposure, and unfunded obligations.

The United States holds the world’s largest official gold reserve, reported at 8,133 tonnes. This is down from over 16,000 tonnes before losing half its reserve between the late 1960s and August 15, 1971.

The tricky part is that since then, no thorough audit of the gold reserve has been conducted, and concerns remain that it may not be as large as claimed. One of Trump’s campaign promises was to initiate an audit of the gold held at Fort Knox. However, as with many things involving Trump, the inspection of Fort Knox has mysteriously never been made public. Naturally, this has only fueled speculation that the U.S. may not hold 8,133 tonnes of gold. Now, three Republican members of Congress have initiated a process to make such an audit a legal requirement. It will be exciting to see whether that legislation passes!

AuAg Funds – Highlights

The AuAg funds reached a new record with SEK 2,340 million in assets under management. We are truly grateful to you, our investors, for the strong net inflows, even during the summer months. Of course, this year’s performance has also contributed to our collective success.

During the month, we made a portfolio update in AuAg Essential Metals, which you can view here. However, the fund of the month is AuAg Precious Core, which delivered the strongest performance in July with +6.88%, placing it among the top 20 funds in Sweden. After gains in May and June, the fund was up as much as 14.1% by July 24, when HedgeNordic also highlighted this strong trend. Then came the final week of July with Trump, the Fed, and volatile markets, which brought the monthly return to +6.88%. Still, the trend seems to have turned!

Global Perspectives with AuAg

As expected, this month—like every month lately—revolves around Trump, tariffs, and the Fed with its non-decisions on interest rates. When the Fed constantly states that it is “data dependent,” one must wonder whether they are needed. After all, a computer could make those decisions.

And what data are they actually using? Often, the “data” used to justify a data-dependent decision later needs to be significantly revised. We’ve long pointed out that this is a problem, but it only seems the house is finally on fire now.

Even though many are growing tired of endless tariff discussions, strong leaders versus weak leaders, the fact remains: if someone wins from this—say, the U.S.—then someone else loses the same amount. It’s a zero-sum game with potentially far-reaching consequences across the globe.

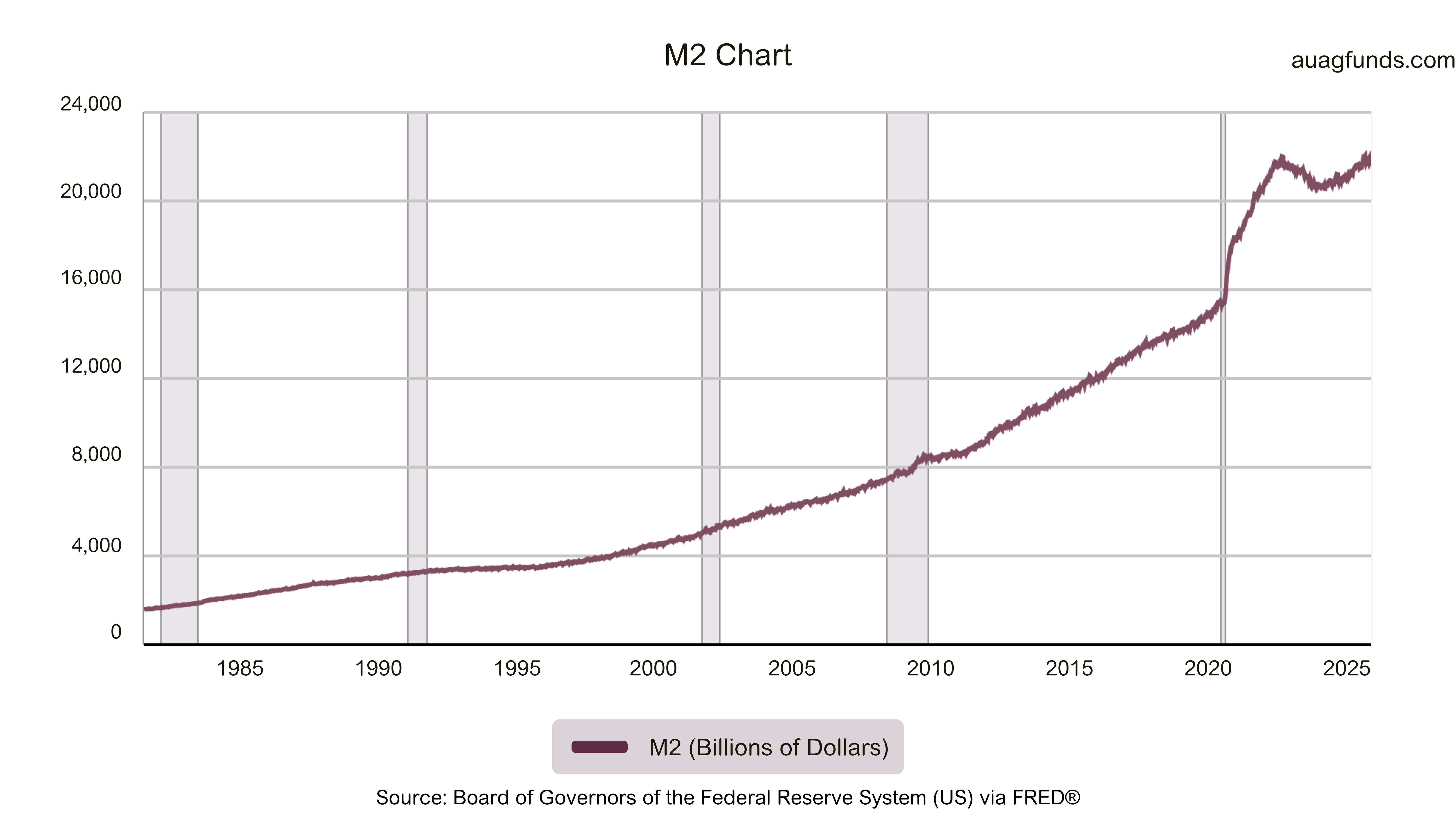

In the U.S., an increasing number of people struggle with mortgage payments, and the “buy now, pay later” trend is surging. We can observe the renewed expansion in the money supply—measured by “M2,” an indicator of total money in the system—which is now rising sharply again. This is a clear sign that we are entering a phase of renewed stimulus and ongoing global monetary inflation.

We also note that valuations in many popular sectors have surpassed all previous historical highs, which could trigger significant concern given the downside risk. On top of that, leveraged investments are now at record levels, adding another layer to the cocktail.

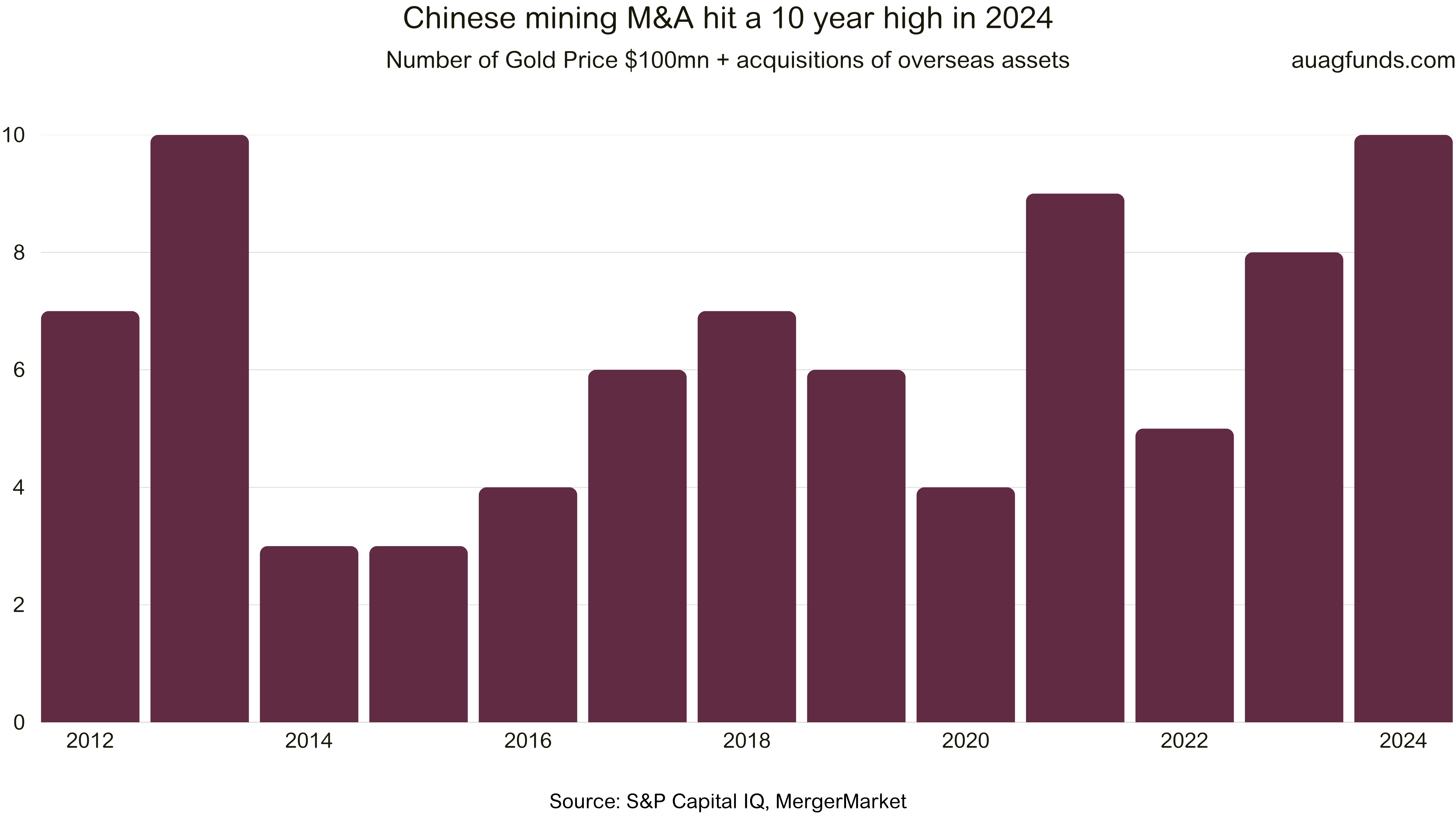

China continues to stimulate its economy and is simultaneously ramping up energy production. Its energy capacity is expanding rapidly, and it seems they understand that the ability to produce energy has always gone hand in hand with human development. China’s aggressive push in the mining sector is also striking. They are focusing more on themselves and positioning for a future where energy and metals will be absolutely critical.

It’s worth noting that the more familiar version of the “Golden Rule” is the noble one: “Do unto others as you would have them do unto you.” We’ll end this monthly letter with some sweet reading about money and a silver standard in Sweden—just in case any of you still have time in the hammock. Now we look forward to an exciting autumn!

Be part of the journey

More than 100,000 investors across Europe have invested in the AuAg funds.

)

)

)

)

Featured content this month

Use our unique "Research Centre" on an ongoing basis to take part in our current view of the market and the macro environment. We communicate all the time. Here are a few media links from the past month:

)

)

)

)